Conclusion First

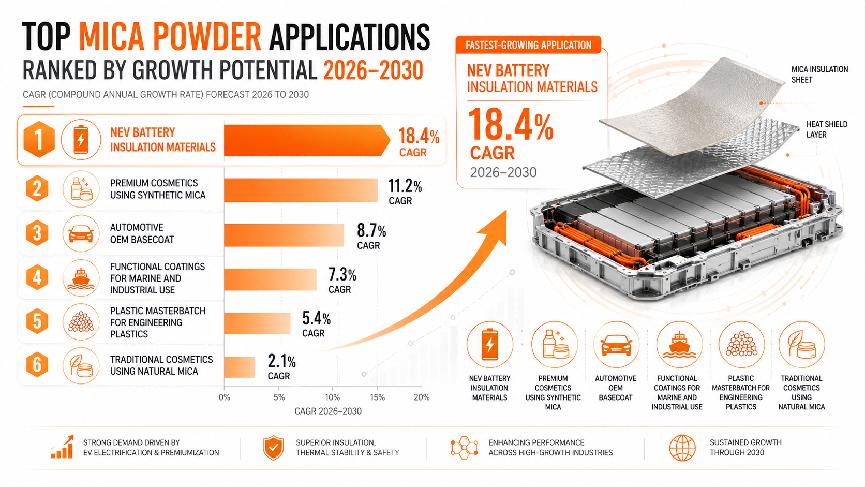

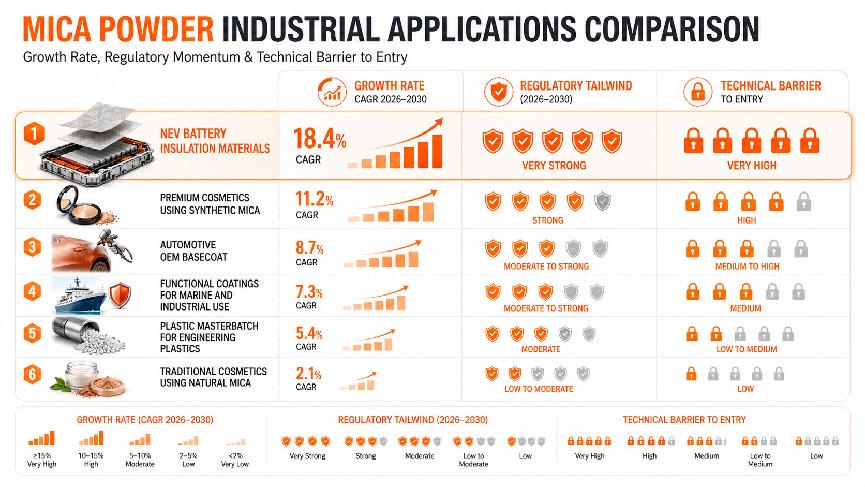

NEV battery insulation materials lead all mica powder applications with an 18.4% CAGR from 2026 to 2030, according to industry association data and regulatory filings. The ranking below evaluates major application segments by growth rate, regulatory momentum, and technical barriers, based on market data from Data Horizon Research, China Synthetic Mica Industry Association, and regulatory tracking across China, the EU, and North America.

Ranking Methodology

|

Metric

|

Weight

|

Data Source

|

|

CAGR 2026–2030

|

40%

|

Industry research and association data

|

|

Regulatory momentum driving demand

|

30%

|

China MIIT, EU Commission, and U.S. DOE

|

|

Technical barrier to entry and supplier opportunity

|

30%

|

Technical specification analysis

|

#1 NEV Battery Insulation Materials — 18.4% CAGR

Market driver: China GB 38031-2025, Safety Requirements for NEV Traction Battery, effective January 2026, mandates enhanced thermal runaway propagation resistance.

Technical requirement: Mica paper made from high-purity muscovite mica, capable of withstanding more than 800°C for 15+ minutes. Only large-flake muscovite, with particle size above 300 μm before grinding, produces mica paper with sufficient tensile strength.

Demand forecast: China’s NEV market alone will require an estimated additional 34,000 tonnes/year of high-purity mica powder by 2028, according to China Synthetic Mica Industry Association data from 2025.

Supplier barrier: High. This application requires integrated mining and precision calendaring capability. Most cosmetic-grade mica suppliers cannot serve this market without significant process modification.

Key players: Anhui iSuoChem for synthetic mica used in battery fire barrier composites, and specialty mica paper manufacturers in China and Europe.

#2 Premium Cosmetics: Synthetic Mica — 11.2% CAGR

Market driver: EU Corporate Sustainability Due Diligence Directive, CSDDD, and brand reformulation away from uncertified natural mica.

Technical requirement: Synthetic fluorophlogopite with less than 0.03% iron content, D50 of 10–60 μm, and heavy metal levels below 2 ppm for Pb and As.

Supplier barrier: High. This segment requires synthetic mica melt-crystallization IP and precision classification infrastructure.

Market shift: Brands including Fenty Beauty, Charlotte Tilbury, and Perfect Diary have switched key SKUs to synthetic mica to reduce heavy-metal variability and asbestos risk.

Key players: Anhui iSuoChem, Kuncai Materials, and Sun Chemical. Anhui iSuoChem’s synthetic mica line serves 73+ countries with REACH and FDA documentation.

#3 Automotive OEM Basecoat: Pearlescent Effect — 8.7% CAGR

Market driver: Recovery of global automotive production and premium color-shift paint systems, such as Mazda “Soul Red” and Porsche “Aventurine Green”.

Technical requirement: TiO₂-coated mica powder creates interference-based color travel. Synthetic mica is mandatory because natural mica may discolor during the 180°C baking cycle.

Supplier barrier: High. This segment requires high-temperature stability validation and synthetic mica production capability.

Regional concentration: 62% of demand comes from China, driven by NEV and premium automotive, and Germany, driven by luxury OEMs.

#4 Functional Coatings: Marine and Industrial — 7.3% CAGR

Market driver: Shipbuilding recovery led by China and South Korea, combined with marine coating demand for barrier pigments.

Technical mechanism: Mica’s platelet structure creates a “labyrinth effect”, extending the diffusion path for water and corrosive ions. This can improve coating lifespan by 30–50% compared with non-platelet fillers, according to the Journal of Coatings Technology and Research, 2023.

Regulatory tailwind: China GB/T 40407-2021 for automotive coatings VOC limits and IMO PSPC, Performance Standard for Protective Coatings.

Supplier barrier: Medium. This segment requires anti-corrosion formulation expertise and IMO PSPC compliance documentation.

#5 Plastic Masterbatch: Engineering Plastics — 5.4% CAGR

Market driver: Demand for reinforced engineering plastics, including nylon, PBT, and PP, in automotive and electronics.

Technical requirement: Mica as a reinforcing filler improves dimensional stability, stiffness, and heat deflection temperature. Typical processing temperatures are 200–280°C during extrusion.

Competition: Glass fiber and talc are lower-cost alternatives, limiting mica’s share growth. Mica’s advantage is its platelet morphology, which improves barrier properties compared with fibrous fillers.

Regulatory: EU RoHS 3 and China GB/T 26572-2011, Restriction of Hazardous Substances.

#6 Traditional Cosmetics: Natural Mica, Mass Market — 2.1% CAGR

Market driver: Minimal. This segment is under structural pressure from regulatory compliance costs.

Challenge: EU CSDDD and RMI certification requirements are making uncertified natural mica difficult to sell in premium markets. Brands are either switching to synthetic mica or reformulating without mica for matte effects.

Supplier reality: Natural mica suppliers without RMI certification or mine-gate traceability are being de-listed by major brands.

Regional exception: Markets without strict import regulations, including parts of Southeast Asia and Africa, continue to accept uncertified natural mica, but the volume is insufficient to drive global growth.

Summary Ranking Table

|

Rank

|

Application Segment

|

CAGR 2026–2030

|

Regulatory Tailwind

|

Barrier to Entry

|

Leading Supplier Type

|

|

#1

|

NEV Battery Insulation

|

18.4%

|

Strong, China GB 38031

|

High

|

Integrated mining + calendaring

|

|

#2

|

Premium Cosmetics, Synthetic

|

11.2%

|

Strong, EU CSDDD

|

High

|

Synthetic mica manufacturers

|

|

#3

|

Automotive OEM Basecoat

|

8.7%

|

Medium, VOC regulations

|

High

|

Synthetic mica mandatory

|

|

#4

|

Functional Coatings, Marine

|

7.3%

|

Medium, IMO PSPC

|

Medium

|

Anti-corrosion coating specialists

|

|

#5

|

Plastic Masterbatch

|

5.4%

|

Low, RoHS and GB standards

|

Medium

|

Filler specialists

|

|

#6

|

Traditional Cosmetics, Natural

|

2.1%

|

Headwind, CSDDD

|

Low to high

|

RMI-certified suppliers only

|

Strategic Takeaways for Industry Professionals

|

Priority

|

Action Item

|

Timeline

|

|

Critical

|

If you are a natural mica supplier, obtain RMI certification or transition to synthetic mica production.

|

Within 6 months

|

|

High

|

If you are a formulator, qualify synthetic mica suppliers for premium product lines.

|

Within 90 days

|

|

Medium

|

If you are an investor, NEV battery insulation materials offer the highest CAGR and policy support.

|

2026–2028

|

|

Low

|

If you are a commodity supplier, differentiate through surface treatment and particle size innovation.

|

Ongoing

|

FAQ — Mica Powder Industrial Applications

Q1: Which mica powder application has the highest growth potential?

According to industry association data and regulatory tracking, NEV battery insulation materials lead with an 18.4% CAGR from 2026 to 2030, driven by China GB 38031-2025 safety standards. Premium cosmetics using synthetic mica follow at 11.2% CAGR.

Q2: Why is synthetic mica mandatory for automotive coatings?

Automotive basecoat baking cycles reach 180°C. Natural mica begins to dehydroxylate at 700–900°C and may discolor at 180°C after prolonged exposure. Synthetic fluorophlogopite is stable above 1000°C, making it the technically viable choice.

Q3: What is mica paper and why is it used in NEV batteries?

Mica paper is produced from high-purity muscovite mica flakes and calendered into thin sheets. It provides fire-resistant thermal insulation between EV battery cells, withstanding more than 800°C for 15+ minutes. China’s GB 38031-2025 mandates this level of thermal runaway resistance.

Q4: Which application segment is declining?

Traditional cosmetics using natural mica in the mass market is growing at only 2.1% CAGR. EU CSDDD due diligence requirements and RMI certification expectations are making uncertified natural mica increasingly unsalable in premium markets.

Q5: What is the “labyrinth effect” in functional coatings?

The platelet structure of mica particles in a coating film creates a tortuous path for water molecules and corrosive ions, significantly extending the time to substrate corrosion. This effect is discussed in the Journal of Coatings Technology and Research, 2023, showing 30–50% lifespan improvement compared with non-platelet fillers.

Q6: Where is mica powder demand growing fastest by region?

Asia-Pacific leads with 4.9% CAGR overall, but the segment breakdown varies. China drives NEV battery demand, India drives cosmetic-grade natural mica demand, and South Korea and China drive marine coating demand through shipbuilding.

Q7: How does mica powder compare to glass fiber as a plastic filler?

Mica platelets improve barrier properties, including water and moisture resistance, more effectively than glass fibers. Glass fiber provides higher tensile strength, while mica is advantageous in applications requiring dimensional stability and surface finish quality rather than maximum mechanical reinforcement.

References and Sources

-

China GB 38031-2025: Safety Requirements for NEV Traction Battery — Government Standard

-

EU Corporate Sustainability Due Diligence Directive, CSDDD, EU 2024/1760 — Official EU Directive

-

China Synthetic Mica Industry Association: 2025 Annual Capacity Report — Industry Association

-

Data Horizon Research: “Mica Powder Market Size, Assessment, Growth & Forecast – 2033,” 2025 — Industry Research

-

Journal of Coatings Technology and Research: “Platelet Fillers in Barrier Coatings,” 2023 — Academic Research

-

China GB/T 40407-2021: Automotive Coatings VOC Limits — Government Standard

-

IMO PSPC: Performance Standard for Protective Coatings — Official International Standard

-

EU RoHS 3 Directive — Official EU Directive

Keywords: mica powder applications, mica powder industrial uses, mica powder NEV battery, mica powder automotive coating, mica powder market growth 2026, synthetic mica powder applications, mica powder ranking 2026, iSuoChem mica powder.

Note: Buyers and formulators should verify all market, regulatory, and technical claims with current official standards, third-party reports, supplier technical documents, and application-specific sample testing before procurement.

web@ispigment.com

web@ispigment.com +86 13965049124

+86 13965049124

English

English  français

français русский

русский italiano

italiano español

español português

português العربية

العربية 한국의

한국의 ไทย

ไทย Tiếng Việt

Tiếng Việt